The Commercial Real Estate Crisis is fast becoming a significant concern as rising office vacancy rates signal an alarming shift in the market. Since the pandemic, demand for office space has plummeted, resulting in vacancies that reach as high as 23% in major U.S. cities, which directly affects property values and overall economic stability. This downturn, combined with stringent lending requirements and high interest rates, has financial experts voicing warnings about potential bank failures due to an influx of commercial real estate loans maturing in the next couple of years. In fact, approximately 20% of the $4.7 trillion in commercial mortgage debt is due this year, amplifying fears of significant impacts on regional economies. As we delve into this situation, the relationship between bank performances and the broader economic landscape becomes increasingly critical to understand in addressing the looming crisis ahead.

As we navigate the ongoing turmoil in the property market, alternate terms such as the commercial property downturn or the office space decline can also encapsulate the current challenges faced by investors and financial institutions alike. The significant rise in unoccupied commercial buildings has left many investors grappling with the aftermath of over-leveraged commitments, threatened further by increasing interest rates. With numerous financial institutions experiencing unprecedented pressure, understanding the broader implications of this commercial property slump is essential for stakeholders. The economic repercussions of such instability could be profound, especially as banks and lending practices begin to tighten in response to potential losses from these high office vacancy rates. Thus, a comprehensive approach towards addressing these challenges may be required to stabilize the commercial real estate landscape.

Understanding Office Vacancy Rates and Their Economic Impact

The high office vacancy rates experienced in urban centers across the United States present a significant challenge to the economy in 2024. With current vacancy rates ranging from 12 to 23 percent, especially in cities like Boston, property values have been adversely affected. This decrease in demand for office space, exacerbated by the pandemic’s long-lasting effects on work habits, raises concerns among economists about the potential ripple effects on the broader economic landscape. As firms grapple with lower revenue from leased properties, the implications for the real estate market can be profound, increasing the likelihood of defaults on real estate loans.

The consequences of these high vacancy rates are multi-faceted. Businesses that own or heavily invest in commercial properties may see their equity eroding, impacting their financial stability. The distress in commercial real estate can lead not only to a decline in rental income but also to a rise in foreclosures and bankruptcies among firms unable to adapt to this shifting market paradigm. As these financial troubles mount, banks may face increased pressure from a wave of bad debt, which could, in turn, tighten the credit conditions for consumers and small businesses.

The Commercial Real Estate Crisis: Causes and Consequences

The looming commercial real estate crisis can largely be attributed to the rapid changes in work dynamics prompted by the COVID-19 pandemic. As businesses reassess their spatial requirements in light of increased remote work, many properties now sit vacant, leading to diminished value across the sector. The aftermath of this scenario may lead to significant challenges for various players in the financial sector. For instance, nearly 20 percent of commercial mortgage debt totaling $4.7 trillion is due this year, raising alarms among investors and banking professionals alike about potential bank failures due to significant delinquencies.

Additionally, the Federal Reserve’s reluctance to lower interest rates further complicates the situation. With higher borrowing costs, recovering investments in real estate becomes increasingly difficult, prompting many lenders to reconsider financing prospects in a volatile market. Real estate loans are particularly vulnerable, as they represent a significant portion of bank assets. Should significant defaults occur, the resulting bank failures could have cascading effects on the economy at large, adversely impacting consumer spending and leading to stricter lending practices.

Interest Rates and Their Role in the Real Estate Landscape

The relationship between interest rates and the commercial real estate market is a pivotal aspect of the ongoing crisis. Following an extended period of low-interest rates, the abrupt increase in borrowing costs has left many investors in a precarious situation. Commercial real estate has become over-leveraged as many borrowers did not plan for an environment of rising rates, resulting in increased vacancies and plummeting property values. Moreover, with office occupancy rates still averaging around 50 percent in major cities, it is clear that demand has not bounced back, amplifying the financial strain on property owners.

Economists like Kenneth Rogoff highlight that the expected stability of long-term interest rates in the coming years paints a complex picture for recovery. Should economic conditions not improve, a continuation of high interest rates may perpetuate the challenges faced by the commercial real estate sector. As a result, financial institutions may find themselves increasingly burdened with high levels of non-performing loans, particularly as real estate values stabilize at lower levels than seen pre-pandemic.

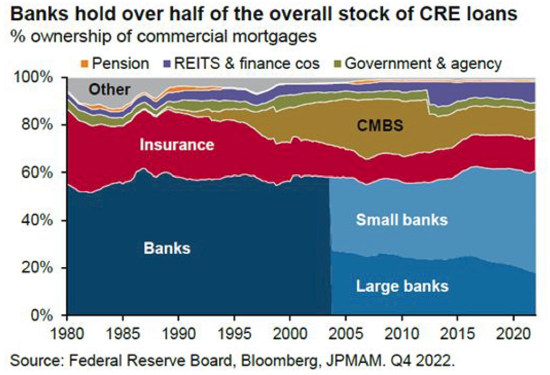

Regional Banks and Their Vulnerability to the Crisis

Regional banks are particularly susceptible to the fallout from the commercial real estate crisis due to their concentration in this sector. Many smaller lenders have invested heavily in real estate loans, and as delinquencies rise, their financial health may become compromised. Unlike larger banks that have the advantage of diversified portfolios, regional banks often lack the same level of regulatory safeguards, making them vulnerable to significant financial distress. The rising vacancies and decreasing real estate values are likely to lead to bankruptcies, further exacerbating the financial instability of these institutions.

As Kenneth Rogoff points out, the risk of regional bank failures may not immediately threaten the broader financial system, but they could influence lending practices and consumer confidence in the affected regions. If these banks encounter severe losses, the constraints on credit could adversely affect local economies, hindering business expansion and consumer spending. While intervention from the Federal Reserve can cushion immediate impacts, it is essential for these banks to navigate this crisis with caution to mitigate long-term consequences.

The Impact of Bank Failures on the Economy

The potential for bank failures stemming from the commercial real estate crisis poses a significant threat to the overall economy. Regional banks that heavily invested in commercial properties may face insolvency if they become overwhelmed by bad debts from declining real estate values. As these banks struggle, their capacity to lend to businesses and consumers could diminish, leading to tighter financial conditions and hampered economic growth. The interconnected nature of the banking sector means that problems in one area can quickly spread, debilitating consumer confidence and creating a more widespread economic downturn.

Furthermore, as the banking sector navigates the repercussions of bad loans, consumers may experience mixed impacts. While some may benefit from an unimpeded stock market, others will feel the pain of higher interest rates and restricted lending. The unique situation highlights the paradox of an economy grappling with challenges in commercial real estate while simultaneously exhibiting overall robust performance in various sectors. However, a severe recession or downturn could potentially alter this balance drastically, intensifying the commercial real estate crisis and its financial repercussions.

The Future of Commercial Real Estate: Prospects and Challenges

Looking ahead, the commercial real estate landscape faces a complex blend of challenges and potential recoveries. As buildings remain vacant and the pressure from maturing loans mounts, industry players will need to adopt innovative strategies to reset their portfolios. The ongoing transition in work culture may prompt a reconsideration of how office spaces are utilized, potentially leading to the conversion of existing structures into mixed-use developments or residential properties. However, the significant hurdles posed by zoning laws and structural limitations must be addressed.

Investors and real estate professionals may also need to reassess their expectations regarding returns on commercial properties in an era of elevated interest rates. The industry may find itself adjusting to a new normal, where higher operational costs and lower demand dictate operational strategies. The future success of commercial real estate depends on the sector’s ability to adapt to these shifting market conditions while navigating the intertwined financial risks that come with high vacancy rates and rising rates.

Consumer Perspectives on the Commercial Real Estate Crisis

From a consumer standpoint, the commercial real estate crisis could lead to heightened uncertainty and adjustments in daily life. As regional banks face potential losses from real estate loans, consumers might experience tighter lending conditions as banks become more risk-averse. This scenario can lead to fewer financing opportunities for small businesses, potentially stifling innovation and local economic development. In turn, these changes could lead to higher consumer prices as businesses pass on increased costs stemming from financial restrictions.

Additionally, the crisis impacts consumers’ perspectives on investing their funds. Many may reevaluate their engagement with real estate investment trusts or related assets due to fears of market volatility. Although some segments of commercial real estate remain lucrative, the overarching narrative surrounds the challenges faced in traditional office spaces. The combined effects of these factors may create a cautious consumer environment where spending decisions are tempered by the perceived stability of the economy.

Government Intervention and Support Measures

Amid the ongoing commercial real estate crisis, discussions about government intervention and support become increasingly relevant. Policymakers are contemplating various measures to ensure that banks remain solvent and that consumers are protected from the fallout of potential failures. This includes examining the regulatory framework to ascertain whether your bank’s risk exposure is mitigated and to fortify financial systems against future shocks. Enhanced scrutiny on the exposure of regional banks to commercial real estate can contribute towards a more resilient financial sector.

Furthermore, targeted measures to support industries affected by high vacancy rates are critical. These could include incentives for property owners to repurpose vacant office spaces or funding for initiatives aimed at mitigating the economic impacts felt in regions most vulnerable to bank failures. Through strategic interventions, governments can foster stability amidst uncertainty and promote a more adaptable approach to navigating the challenges presented by the ongoing crisis.

Expectations for Recovery in the Commercial Real Estate Sector

Looking to the future, expectations for recovery in the commercial real estate sector hinge on various interrelated factors, including economic growth and interest rate fluctuations. As some experts envision a stabilization of long-term interest rates, there is hope that this could foster a more favorable environment for refinancing existing debts. However, sustaining growth in the face of rising operational costs and persistent vacancy rates will require strategic adjustments from both property owners and investors.

Ultimately, a commitment to innovation and flexibility will be essential in transitioning towards a post-crisis landscape. The investment community must be prepared to shift its approach, recognizing that the landscape of work and real estate needs to evolve. Successful navigation of the road ahead will depend on the ability of all market participants to respond effectively to changing demands, ensuring that commercial real estate can adapt to the expectations of a modern economy.

Frequently Asked Questions

How will high office vacancy rates impact the economy during the Commercial Real Estate Crisis?

High office vacancy rates are likely to adversely affect the economy during the Commercial Real Estate Crisis by depressing property values, leading to financial strain on investors and banks holding commercial real estate loans. As demand for office space remains low, companies may scale back expansions, impacting job creation and consumer spending, which can further slow economic growth.

What role do interest rates play in the current Commercial Real Estate Crisis?

Interest rates are a crucial factor in the current Commercial Real Estate Crisis, as they influence borrowing costs for real estate loans. The Federal Reserve’s current hesitation to lower interest rates adds pressure to an already strained market, making it difficult for property investors to refinance their debts. This could lead to increased delinquencies and potential bank failures if property values continue to decline.

Are bank failures a significant risk due to the Commercial Real Estate Crisis?

Yes, bank failures are a significant risk associated with the Commercial Real Estate Crisis, especially among regional banks heavily invested in commercial real estate loans. If a wave of delinquencies occurs as properties lose value, these banks may see their financial stability jeopardized, potentially leading to a cycle of consolidation or forced bailouts.

What economic impacts can result from rising office vacancy rates during the Commercial Real Estate Crisis?

Rising office vacancy rates during the Commercial Real Estate Crisis can lead to decreased property values and rental income, affecting local economies. Increased vacancy can also deter new business investments, leading to slower job growth and reduced consumer confidence, which hampers overall economic performance.

How are real estate loans affected by the Commercial Real Estate Crisis?

Real estate loans are significantly affected by the Commercial Real Estate Crisis as many loans are coming due amidst high vacancy rates and declining property values. Lenders may face losses if borrowers default, resulting in tighter lending conditions and higher interest rates, further complicating the financial landscape.

What measures can be taken to mitigate the effects of the Commercial Real Estate Crisis?

To mitigate the effects of the Commercial Real Estate Crisis, potential measures include adjusting interest rates to stimulate refinancing opportunities, implementing targeted financial support for struggling banks, and encouraging investment in adaptive reuse of vacant office spaces to meet housing demands and rejuvenate urban areas.

How do economic factors contribute to the Commercial Real Estate Crisis?

Economic factors such as high interest rates, decreased demand for office space due to remote work trends, and the resulting decline in occupancy rates contribute to the Commercial Real Estate Crisis. These elements create a challenging environment for property owners, leading to financial instability among investors and lenders in the commercial real estate sector.

What is the potential for another financial crisis stemming from the Commercial Real Estate Crisis?

While the Commercial Real Estate Crisis poses serious risks, it is not necessarily indicative of another financial crisis like that of 2008. However, if conditions worsen and significant delinquencies occur, particularly among smaller banks, it could lead to broader economic impacts and financial instability if not managed appropriately.

How does the current economic climate affect the Commercial Real Estate Crisis?

The current economic climate, characterized by solid employment levels and a booming stock market, offers some buffer against the full effects of the Commercial Real Estate Crisis. However, persistent high interest rates and significant losses in commercial property values could still have detrimental effects, particularly on regional banks and local economies.

Will consumers experience direct impacts from the Commercial Real Estate Crisis?

Yes, consumers may experience direct impacts from the Commercial Real Estate Crisis, such as diminished pension fund performance due to losses in commercial real estate investments. Furthermore, if regional banks struggle due to bad loans, tighter lending practices could lead to fewer loans available for consumer mortgages and businesses, hindering economic activity.

| Key Points | Details |

|---|---|

| High office vacancy rates | Current vacancy rates range from 12% to 23% in major US cities, affecting property values. |

| Surge in commercial real estate loans | 20% of $4.7 trillion in commercial mortgage debt is due in 2024, raising concerns about market stability. |

| Potential impact on banks | Some banks may face significant losses; smaller banks may be more vulnerable due to lower regulations. |

| Long rates outlook | Experts believe interest rates may remain high over the next decade, affecting refinancing opportunities. |

| Continued demand issues | Pandemic-induced demand for office space remains low; some areas of real estate market are still stable. |

| Bank system resilience | Larger banks are more diversified and financially stable; regional banks may face challenges. |

Summary

The Commercial Real Estate Crisis poses significant risks to the U.S. economy, primarily due to the high office vacancy rates and a substantial amount of commercial mortgage debt scheduled to mature. While experts express concerns about regional banks potentially facing significant losses, the broader banking system remains resilient. The ongoing challenges in commercial real estate might not lead to a repeat of the 2008 financial crisis, but they indicate a slow-moving deterioration that could have lasting effects on the economy. Strategies for mitigating these risks will be crucial as the market seeks to navigate this turbulent landscape.