Corporate tax cuts, particularly those enacted by the 2017 Tax Cuts and Jobs Act (TCJA), have ignited passionate debates among policymakers and economists alike. A significant reduction in corporate tax rates from 35% to 21% promised to stimulate economic growth, attract business investments, and provide a crucial boost to job creation. However, recent analyses, notably a study by Gabriel Chodorow-Reich, have challenged the effectiveness of these tax cuts by highlighting their limited positive impact on wages and overall tax revenue. As key provisions of the TCJA face expiration in 2025, discussions surrounding the future of corporate tax policy are heating up, with both Republicans and Democrats pushing for contrasting reforms. Understanding the ramifications of these corporate tax rate changes is vital for voters and legislators as they navigate the complexities of economic growth and taxes in the upcoming election cycle.

The ongoing discussion about reducing taxes on businesses, often referred to as corporate taxation reforms, has significant implications for the economy and public policy. The 2017 Tax Cuts and Jobs Act stands at the center of this dialogue, showcasing the potential for tax relief to influence corporate behaviors, investment decisions, and the broader economic landscape. As researchers like Gabriel Chodorow-Reich explore the effects of these fiscal strategies, it becomes increasingly clear that the relationship between tax cuts and economic vitality is not straightforward. With legislative measures set to expire soon, the looming tax debates represent not just a financial calculation but a pivotal moment that could reshape economic incentives and fiscal policies for years to come. By evaluating the impact of corporate tax alterations, we can uncover valuable insights into effective governance and sustainable economic growth.

Understanding the 2017 Tax Cuts and Jobs Act

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in U.S. tax policy, notably lowering the corporate tax rate from 35% to 21%. This reduction aimed to make American businesses more competitive globally, especially as other countries had started to lower their corporate tax rates significantly. According to the findings of Gabriel Chodorow-Reich, the TCJA resulted in a modest 11% increase in capital investments; however, the optimistic projections regarding wage increases and overall economic growth have been met with skepticism. The act’s implications led to extensive debates on whether the tax cuts ultimately stimulated the economy as intended.

While proponents of the 2017 Tax Cuts and Jobs Act argued that lowering corporate tax rates would encourage companies to reinvest in the economy, empirical evidence has shown a more complex picture. The expected surge in investment did occur, but the direct link between tax cuts and substantial wage growth remains dubious. Chodorow-Reich’s analysis highlighted that the initial corporate investment boost did recover significantly after a sharp decline in tax revenues, but this recovery is not fully attributed to the TCJA. Instead, it raised further questions about the real impact of corporate tax restructures in a fluctuating economic landscape.

The Impact of Corporate Tax Cuts on Economic Growth

The relationship between corporate tax cuts and economic growth is a contentious topic among economists and policymakers. The fundamental argument presents that reducing tax liabilities for corporations should lead to increased investment, job creation, and ultimately, higher wages for employees. However, the empirical data, as outlined in the Gabriel Chodorow-Reich study, casts doubt on this assumption. The TCJA’s significant cuts did produce a rise in capital investments but failed to generate the high levels of wage growth initially predicted. This raises an important question: do corporate tax cuts truly spur economic growth or do they merely benefit business profits?

Chodorow-Reich’s findings indicate that while some economic benefits materialized, they were not as substantial as proponents suggested. For instance, although there was an uptick in corporate investments, the anticipated wage growth did not align with the projections made prior to the implementation of the TCJA. The study emphasizes the need for a more nuanced understanding of how corporate policy influences both investment and working-class earnings. As discussions swirl around future tax policies, it’s crucial to critically assess whether further corporate tax reductions will genuinely enhance economic growth or simply exacerbate existing disparities in wealth distribution.

Corporate Tax Rate Changes: What Lies Ahead?

As discussions around tax reform heat up in 2025, the status of corporate tax rates continues to be a pivotal issue. With key provisions of the TCJA set to expire, policymakers are analyzing whether to maintain the lower corporate rates or to reinstate higher taxes to address budget deficits and invest in social programs. The previous arguments advocating for tax cuts underscore a belief in their ability to catalyze business investments and job creation. However, the findings from leading studies, including Chodorow-Reich’s analysis, underscore the importance of reevaluating these assumptions for future tax policies.

The debate extends to both major political parties as they argue over the best approach. Democrats may advocate for an increase in corporate tax rates to redistribute wealth and fund public projects, while Republicans continue to support the notion that lower taxes will fuel economic momentum. Despite the polarized opinions, a careful analysis of the TCJA’s impact reveals that mere rate cuts may not lead to the robust economic benefits touted. Going forward, it will be critical to weigh the implications of corporate tax rate changes in order to craft balanced fiscal policies that adequately address both revenue needs and economic growth.

The Gabriel Chodorow-Reich Study: Key Findings and Implications

The recent analysis by Gabriel Chodorow-Reich provides a comprehensive review of the impact of the 2017 Tax Cuts and Jobs Act on corporate income and investment behaviors. One of the most significant takeaways from his research is that, while corporate tax cuts did lead to some investment increases, the overall impact was less dramatic than many had anticipated. Chodorow-Reich’s work brings forth critical data that should inform future debates on tax reform by emphasizing that cutting corporate tax rates alone does not guarantee economic prosperity.

Additionally, the study highlights the cost-effectiveness of expiring tax provisions aimed at promoting capital investment, suggesting that such targeted measures may yield better outcomes than broad rate reductions. The focus on specific incentives, such as expensing provisions for new capital investments, could play a pivotal role in future discussions about how to stimulate the economy without exacerbating tax revenue losses. Chodorow-Reich’s findings could thus serve as an essential framework for shaping more effective tax policies moving forward.

Debate Over Corporate Tax Policies in Election Years

As the expiration of significant provisions from the 2017 Tax Cuts and Jobs Act approaches, it is evident that corporate tax policies will be a critical front in the upcoming election campaigns. Candidates from both major political parties are leveraging the implications of the TCJA to shape their platforms and appeal to voters. For example, Vice President Kamala Harris advocates for raising corporate tax rates as a means to finance social initiatives, contrasting sharply with former President Donald Trump’s call for further reductions to drive economic growth. This divisive landscape illustrates how corporate tax policies have become a focal point of economic discourse in election years.

The political stakes surrounding corporate tax reforms are heightened further by growing public awareness of income inequality and economic disparities. The dialogue surrounding the TCJA has opened avenues for voters to consider how tax policies affect not only corporate entities but also average citizens. As investigations, such as Chodorow-Reich’s, illuminate the real-world implications of corporate tax cuts, it is likely that the electorate will demand more accountability and informed decision-making from their representatives regarding future tax legislation.

The Role of International Competition in Corporate Tax Policy

International competition plays a crucial role in shaping national corporate tax policies. Economists like Gabriel Chodorow-Reich have noted that the U.S. corporate tax system has faced growing pressure from other developed nations, many of which have reduced their corporate tax rates to attract foreign investments. This competitive landscape was a driving force behind the establishment of the TCJA. As businesses increasingly operate on a global scale, policymakers must consider how tax structures affect the ability to compete internationally.

The dynamic nature of the global market means that maintaining an attractive corporate tax environment is essential for the resilience of the U.S. economy. The findings from recent studies suggest that simply lowering tax rates may not suffice to retain competitiveness, as businesses also respond to other factors like infrastructure, workforce quality, and political stability. Thus, ongoing debates about corporate tax cuts must evaluate not only the immediate economic impacts but also the longer-term implications for the U.S. as it navigates a rapidly evolving international economy.

Evaluating the Effectiveness of Corporate Tax Incentives

The effectiveness of corporate tax incentives remains a hot topic among economists and policymakers. The premise of such incentives, including those embedded in the TCJA, is to stimulate growth by encouraging businesses to invest in capacity and workforce. However, the study by Chodorow-Reich and his colleagues reveals that while these incentives have resulted in some positive outcomes, such as increased investment, they have not met the more ambitious goals set during the tax reform discussions.

In light of this, it is essential to reassess how tax incentives can be structured to improve efficacy. Instead of blanket rate reductions, targeted incentives that address specific investment types may yield more significant results. As the landscape shifts, stakeholders must engage in a pragmatic evaluation of corporate tax policies to identify which mechanisms successfully promote growth while ensuring revenue stability. The conversation about corporate tax incentives must therefore evolve beyond mere rate considerations to consider their broader economic impact.

Future Considerations for Corporate Tax Reforms

Looking forward, the forthcoming revisions to corporate tax policies must consider the lessons learned from the TCJA’s application. As Gabriel Chodorow-Reich’s research indicates, the purported benefits of tax cuts must be scrutinized to ensure they genuinely align with the goals of fostering economic growth and innovation. Future reforms could benefit from adopting a balanced approach that incorporates both competitive tax rates and strategic incentives aimed at specific sectors or objectives.

Moreover, legislators are encouraged to engage in comprehensive evaluations of the long-term repercussions of tax changes, particularly how they influence corporate behaviors and the economy as a whole. By analyzing past outcomes, including revenue implications and investment trends, lawmakers can establish a more informed path forward that not only addresses budgetary needs but also emphasizes sustainable economic development. As discussions around corporate tax reforms evolve, stakeholders must prioritize data-driven approaches that enhance accountability and transparency in fiscal policies.

Comparative Analysis: U.S. and Global Corporate Tax Rates

A comparative analysis of U.S. corporate tax rates against those of other developed nations reveals significant disparities that influence economic policymaking. Historically, the U.S. maintained one of the highest corporate tax rates globally, which has been a point of contention as other countries sought to become more attractive for business. According to Chodorow-Reich’s insights, the 2017 Tax Cuts and Jobs Act was a response to these competitive pressures, yet the resulting shifts have prompted ongoing debates about adequacy and competitiveness in the global market.

As many nations have adopted lower corporate tax rates, the U.S. must navigate the complexities of formulating tax policies that not only attract investment but also sustain public resources. The implications of tax rate structures extend beyond mere comparison; they influence cross-border investment flows and the strategic decisions made by multinational corporations. Consequently, moving forward, U.S. taxation strategies should aim to balance competitiveness while ensuring that sufficient revenue generation supports national priorities.

Frequently Asked Questions

What are corporate tax cuts as outlined in the 2017 Tax Cuts and Jobs Act?

Corporate tax cuts refer to the reduction in the corporate income tax rate mandated by the 2017 Tax Cuts and Jobs Act (TCJA), which lowered the federal corporate tax rate from 35% to 21%. This legislation was enacted to stimulate economic growth by encouraging business investment and increasing competitiveness in a global market.

How does the 2017 Tax Cuts and Jobs Act impact corporate tax rates?

The 2017 Tax Cuts and Jobs Act significantly impacted corporate tax rates by permanently reducing the rate to 21%, which was intended to boost investment from companies and enhance overall economic growth. This reduction aimed to make U.S. corporate rates more competitive compared to other developed countries, which had been lowering their rates.

What insights does the Gabriel Chodorow-Reich study provide on corporate tax cuts?

The Gabriel Chodorow-Reich study analyzes the effects of corporate tax cuts under the 2017 Tax Cuts and Jobs Act, revealing that while there were modest increases in wages and business investments, these gains were insufficient to compensate for the significant decline in tax revenue. The study suggests that the anticipated results from tax cuts may not fully align with real-world data.

What is the relationship between corporate tax cuts and economic growth, as per research findings?

Research indicates that while corporate tax cuts, such as those in the TCJA, were expected to drive economic growth, evidence shows that the actual increase in wages and investment was moderate. The discussion remains contentious, with some studies suggesting nominal benefits, while others highlight that substantial increases in corporate profits were not entirely due to tax cuts alone.

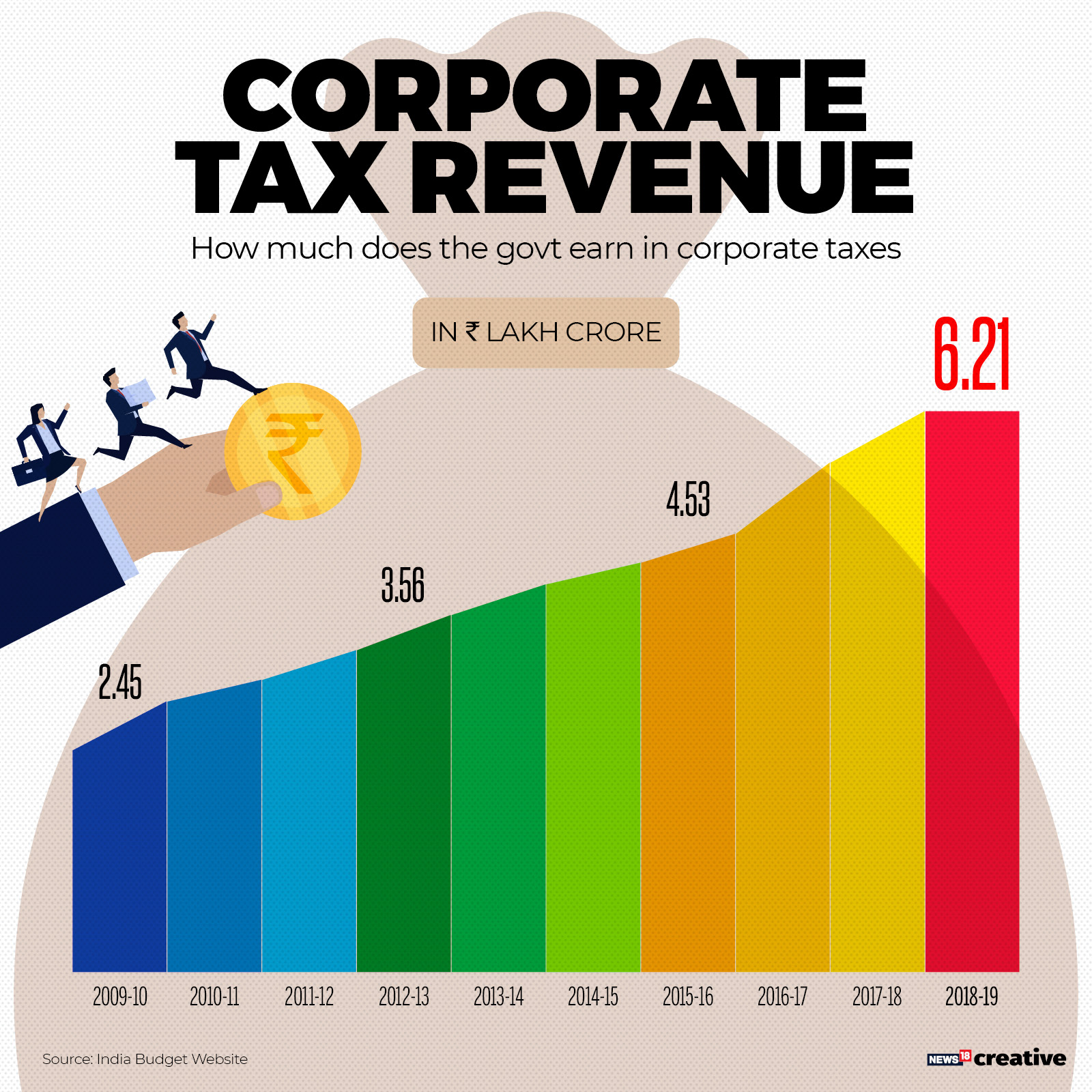

How did the corporate tax cuts from the TCJA affect corporate tax revenues in the U.S.?

Following the implementation of the TCJA, corporate tax revenues initially fell by approximately 40%. However, this revenue began to recover around 2020 as corporate profits surged, exceeding pre-pandemic predictions, showing that firms were still able to generate wealth despite lower tax rates.

What lessons can be learned from the corporate tax cuts of the Tax Cuts and Jobs Act?

The lessons from the corporate tax cuts of the TCJA suggest that while lower tax rates can incentivize investment, they may not automatically result in proportional increases in wage growth or tax revenue. It highlights the complexity of corporate tax policy and the need for balanced approaches to encourage both business investment and stable tax revenues.

Are corporate tax cuts effective in driving business investment according to recent studies?

Recent studies, including findings from the Gabriel Chodorow-Reich analysis, suggest that while corporate tax cuts can stimulate some business investment, targeted measures like expensing provisions may drive investment more effectively. The nuances in data indicate that reductions in corporate tax rates alone do not guarantee higher investment levels.

What are the proposed future changes to corporate tax rates in light of the 2017 tax cuts?

Proposed future changes to corporate tax rates suggest a potential increase to fund social initiatives, as discussed by political leaders ahead of upcoming elections. Lawmakers may consider restoring certain expensing provisions to promote investment, even as debates over raising the corporate tax rate continue.

| Key Points |

|---|

| The 2017 Tax Cuts and Jobs Act (TCJA) reduced corporate tax rates from 35% to 21%. The law is set to face expiration in 2025, leading to campaign discussions around corporate taxes. |

| The TCJA was aimed at stimulating economic growth, yet it prompted debates over its effectiveness, especially regarding wage increases and investment. |

| Gabriel Chodorow-Reich’s analysis suggests that while corporate investment increased by 11%, the tax cuts did not significantly boost wages as initially projected. |

| Corporate tax revenue initially decreased by 40%, but recovered beyond expectations starting in 2020, mainly due to increased business profits. |

| The upcoming 2025 tax discussions could involve reinstating expensing provisions while potentially raising statutory rates to encourage investment and revenue. |

Summary

Corporate Tax Cuts have emerged as a pivotal topic in the ongoing tax debate as the expiration of key provisions from the 2017 Tax Cuts and Jobs Act approaches in 2025. The TCJA significantly altered the corporate tax landscape, sparking partisan discussions about the effectiveness of lowering taxes to stimulate growth. Analysis shows that while some moderate increases in investment were noted, the anticipated wage growth did not materialize to the extent expected. As the political climate heats up, the reevaluation of these tax policies is crucial for forming informed economic strategies moving forward.