The economic impact of climate change is rapidly emerging as one of the most critical issues of our time, as recent studies reveal projections significantly more daunting than past estimates. Researchers have found that every 1°C rise in global temperatures could result in a staggering 12 percent decline in global GDP, painting a stark picture of the cost of climate change to economies worldwide. This decline in productivity not only threatens individual nations but poses a serious risk to the growth of the global economy, leaving policymakers and business leaders grappling with the realities of climate change economics. As organizations race to implement decarbonization policies, the implications for economic projections related to climate change continue to grow increasingly severe. Understanding these dynamics is essential as we forge a path toward sustainable economic resilience in the face of looming environmental challenges.

The financial repercussions of climate disruption are becoming increasingly evident, with emerging research indicating stark declines in economic performance due to rising global temperatures. As economies grapple with the tangible effects of environmental degradation, the interplay between climate change and economic viability must be addressed urgently. With forecasts suggesting that the global GDP could suffer significant losses, the necessity for robust strategies to mitigate these risks through effective decarbonization and adaptive policies is clearer than ever. The urgency to act highlights the intertwined fate of environmental health and economic prosperity, necessitating a re-evaluation of how we approach both climate stability and financial growth. In essence, we face a pivotal moment where addressing climate challenges could dictate future economic trajectories on both local and global scales.

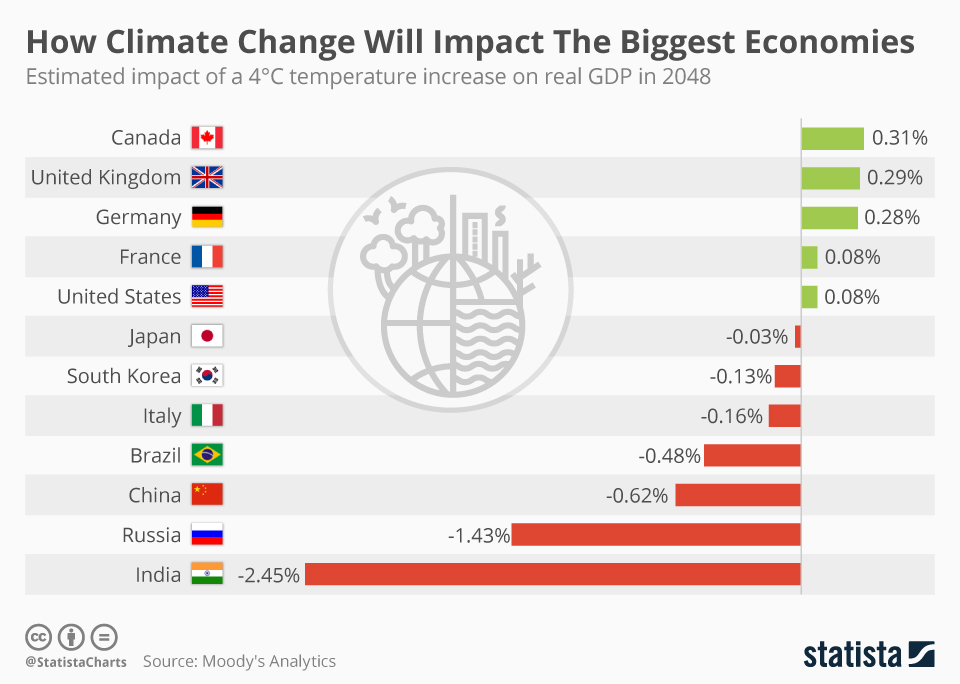

The Economic Impact of Climate Change

Climate change poses a significant threat to global economies, affecting everything from productivity to spending habits across nations. Recent studies have revealed that an increase in global temperatures by just 1°C could result in a staggering 12% reduction in global GDP. This alarming perspective highlights the urgency for countries to rethink and reshape their economic forecasts to account for the escalating damages associated with climate change. As extreme weather events become more frequent and severe, the economic predictions that previously deemed climate change impacts as moderate are no longer applicable.

The economic impact of climate change extends beyond mere GDP figures; it encompasses a broader scope of financial consequences that can impact millions of individuals and businesses worldwide. With projections indicating severe economic repercussions from an additional rise in temperature, it becomes increasingly critical for policymakers to understand and factor these estimates into long-term economic planning. The real cost of climate change must include both its immediate effects on industries and the longer-term impacts on social welfare, highlighting the urgent need for substantial investment in adaptation and mitigation efforts.

Revising Climate Change Economics: New Perspectives

Traditional approaches to climate change economics have often underestimated the potential costs associated with rising global temperatures. The recent study led by Adrien Bilal and Diego R. Känzig reveals a stark revision in the understanding of climate change’s economic toll, suggesting a figure that is six times larger than earlier estimates. This shift challenges existing frameworks that relied on national temperature variations for economic forecasting, underscoring the necessity of integrating global temperature dynamics into economic models for more accurate projections.

This innovative perspective on climate change economics is paramount as it highlights the interconnectedness between climate factors and economic stability. Utilizing extensive data sets spanning over a century, the study illustrates how overlooked elements, such as extreme weather fluctuations, can drastically alter economic outcomes. By recognizing that every degree of warming can lead to substantial economic losses, we can better prepare and implement effective decarbonization policies that not only address climate concerns but also foster economic resilience.

Cost of Climate Change: Understanding the Figures

The financial implications of climate change are profound, as underscored by recent calculations revealing a ‘social cost of carbon’ that far exceeds previous evaluations. The study identifies a cost of $1,056 per ton of carbon emissions, significantly higher than the $185 per ton figure derived from conventional approaches. This stark difference emphasizes the need for accurate quantification of climate change impacts when devising economic strategies, positioning policymakers to make informed decisions about carbon pricing and emissions reduction initiatives.

Understanding the cost of climate change is essential not only for economic modeling but also for shaping effective policy. By establishing a more realistic social cost of carbon, countries can evaluate the economic viability of decarbonization projects, making the case for sustainable practices that will mitigate future losses. The study’s findings bolster the argument that transitioning to a low-carbon economy through comprehensive decarbonization policies is not just an environmental imperative, but also an economically sound strategy that benefits national economies.

Economic Projections for a Warming World

Projecting the economic future amid rising temperatures presents a significant challenge for economists and policymakers alike. This recent analysis sheds light on the correlation between global temperature increases and economic downturns, suggesting that an additional 2°C rise could halve global output and consumption. Such drastic projections compel nations to reevaluate their current economic models and implement proactive measures to address climate-induced challenges that could exacerbate economic instability.

As we navigate the complexities of economic projections in a warming world, it becomes clear that adaptation strategies must be integrated into long-term planning. While growth may continue, the refrain that productivity inherently ties with climate stability rings true. Policymakers are therefore urged to innovate adaptive mechanisms that not only respond to climate variations but also nurture economic growth, ensuring that future generations can thrive in a changing world.

Decarbonization Policies and Economic Viability

Decarbonization policies are increasingly cited as essential to mitigating the economic fallout attributed to climate change. The recent findings present a strong case for significant investments in clean energy technologies, as the cost-benefit analysis reveals that these interventions are economically advantageous for major economies. With a projected social cost of carbon that highlights the dire economic need for action, the alignment of policy and economic incentives is more crucial than ever.

Investing in decarbonization not only addresses environmental concerns but also spurs job creation and supports economic resilience. By shifting toward sustainable practices, governments can catalyze a green economy that facilitates innovation and reduces dependence on carbon-intensive industries. Such measures ensure that economies remain robust while striving to achieve climate goals, demonstrating that a sustainable future is both an ecological necessity and an economic opportunity.

The Role of Technological Innovation in Climate Economics

Technological innovation is a critical driver of economic growth and has the potential to play an integral role in counteracting the adverse effects of climate change. With advancements in renewable energy, energy efficiency, and carbon capture technologies, the economy can transition away from fossil fuel reliance while enhancing productivity. This transformative approach not only curtails carbon emissions but also opens up new avenues for economic development.

As we embrace cutting-edge technologies, it is crucial to consider their implications on climate change economics. Investments in research and development can lead to breakthroughs that effectively lower the social cost of carbon, changing the narrative around climate policy from a burden to an opportunity. By fostering an ecosystem that encourages innovation, we can ensure a sustainable economic future that aligns with our climate goals, driving growth while safeguarding our planet.

Assessing the Long-Term Costs of Inaction

The consequences of inaction in the face of climate change are dire and could lead to significant long-term economic losses. Failing to address rising temperatures allows for the amplification of extreme weather events, which not only disrupt productivity but also strain public resources and infrastructure. The repercussions on global GDP, projected to decline dramatically with each passing degree of warming, underscore the financial imperative to act decisively.

Assessment of long-term costs emphasizes the necessity for immediate action in implementing climate policies. As economists continue to refine projections and incorporate the realities of climate impacts on economic systems, the narrative shifts from viewing climate action as an expense to recognizing it as an investment in economic stability and resilience. Preparing for an uncertain future involves understanding these costs and committing to proactive measures that protect both economies and the environment.

Integrating Climate Data into Economic Models

The integration of climate data into economic models is a vital element in producing accurate forecasts regarding the costs associated with climate change. Traditional economic models have often overlooked the significant variables introduced by climate fluctuations, resulting in optimistic projections that underestimate risk. By adopting a comprehensive approach that includes global temperature trends and extreme weather patterns, economists can develop more accurate assessments of climate impacts on national and global economies.

Enhancing our economic models to reflect climate realities allows for more informed decision-making among policymakers, ensuring that necessary adaptations and interventions are rooted in empirical evidence. With a clearer understanding of the economic implications of climate change, nations can forge pathways for resilient economies that can withstand the challenges posed by environmental shifts. This integrative approach not only enhances predictive accuracy but also fosters collaboration between climate science and economic policies.

Global Collaboration: A Framework for Climate Economics

In an interconnected world, global collaboration is imperative to tackle the economic ramifications of climate change effectively. Collective efforts toward knowledge sharing, technology transfer, and joint policy initiatives can unify nations in their response to climate threats. Through global financial partnerships and alliances, countries can pool resources and expertise, fostering innovation in climate adaptation and mitigation strategies on a larger scale.

Such collaboration can also help standardize economic assessments of climate change, enabling consistent measurements of the social costs of carbon across borders. By establishing frameworks for cooperation, the global community can respond more effectively to climate challenges, ensuring that economic growth does not come at the expense of environmental sustainability. Ultimately, united action will facilitate a shift toward greener economies, while addressing the shared risks posed by climate change on a global scale.

Frequently Asked Questions

What is the economic impact of climate change on global GDP?

The economic impact of climate change on global GDP is severe, with projections suggesting that each additional 1°C increase in global temperature may lead to a staggering 12 percent decline in global gross domestic product (GDP). This means that the cost of climate change could drastically hinder global economic growth, underscoring the urgent need for effective climate policies.

How do economic projections for climate change differ from previous estimates?

Recent economic projections for climate change indicate that the potential costs are six times larger than earlier estimates. This disparity arises from factors like increased extreme weather events and their effects on productivity and capital, suggesting that traditional models may underestimate the economic impact of climate change.

What are the long-term economic projections related to climate change?

Long-term economic projections suggest that if global temperatures rise by 2°C by the end of the century, output and consumption could plummet by 50 percent, representing an economic loss greater than the Great Depression. This emphasizes the critical need for immediate action to mitigate climate change’s economic fallout.

How do decarbonization policies affect the economics of climate change?

Decarbonization policies are essential for addressing the economic impact of climate change, as they have been shown to provide significant cost benefits. For instance, the social cost of carbon recalculated using new methodologies reveals that decarbonization efforts can pass cost-benefit analyses, making them economically viable for large economies like the U.S. and the European Union.

What is the cost of climate change per ton of carbon?

Recent studies estimate the social cost of carbon at $1,056 per ton using updated climate and economic models, compared to much lower local estimates of around $185 per ton. This reflects the true economic impact of climate change and highlights the importance of investing in decarbonization policies.

How does climate change economics account for extreme weather events?

Climate change economics increasingly incorporates the rise in extreme weather events, which are correlated with global temperature increases. Traditional economic models often overlook these factors, leading to an underestimation of the economic impacts of climate change, particularly on industries reliant on stable weather patterns.

What role does technological innovation play in climate change economics?

Technological innovation contributes to economic growth; however, it can also increase greenhouse gas emissions, aggravating climate change. In the context of climate change economics, understanding the balance between innovation’s economic benefits and its environmental costs is crucial for developing effective decarbonization strategies.

What is the relationship between climate change and productivity declines?

Studies have shown that climate change can lead to significant declines in productivity, particularly in sectors vulnerable to temperature increases. The new analysis suggests that the linkage between rising global temperatures and productivity downturns is stronger than previously predicted, highlighting the need for proactive climate policies.

| Key Point | Details |

|---|---|

| New Economic Estimates | Recent analysis projects that each 1°C increase in global temperature will lead to a 12% decline in global GDP. |

| Historical Data Used | The research integrated weather and economic records from the last 120 years across 173 countries. |

| Comparison to Previous Estimates | The new model’s findings are six times greater than earlier predictions regarding the economic impact of climate change. |

| Social Cost of Carbon | The social cost of carbon is estimated at $1,056 per ton globally using the new methodology, compared to just $185 per ton in previous assessments. |

| Implications for Policy | The findings suggest that current decarbonization policies, like those in the Inflation Reduction Act, are economically viable at an estimated cost of $95 per ton. |

Summary

The Economic Impact of Climate Change is a pressing issue that highlights the need for a significant reevaluation of previously held beliefs about the effects of global warming on the economy. Recent studies indicate that rising temperatures could lead to severe economic losses, far beyond earlier estimates. As global temperatures increase, there is a clear expectation of substantial declines in GDP, pointing to an urgent need for effective climate action. This research underscores the critical link between environmental sustainability and economic resilience, reinforcing the need for policies that target carbon emissions to avoid catastrophic economic consequences.